Credit Card Chargeback Laws / How To Manage False And Fraudulent Chargebacks. Throughout • remove conditions under chargeback reason 4837 (no cardholder authorization), which had allowed an acquirer to provide brand new information of merchant name or date as a While credit card companies can address fraud internally, a chargeback can be requested in cases when you have legitimately authorized payment for goods or services that were either not received or were not delivered as described. To fight a chargeback, you have to respond to it formally. Section 75 makes the credit card provider jointly liable with the retailer if something goes wrong. If the card scheme rules don't provide for a chargeback, the bank (or credit union) is not required to seek one.

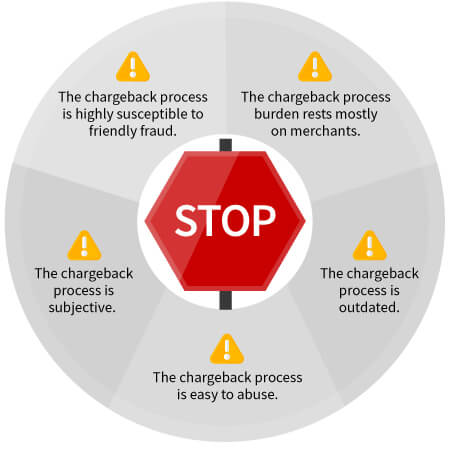

The credit card industry strongly favors cardholders in the majority of cases, which can make it nearly impossible for legitimate business owners to fully protect themselves from invalid chargebacks. Chargeback is not enshrined in law but is part of scheme rules, which participating banks subscribe to. Credit card companies each have their own rules for responding to chargebacks, so first, find out which ones apply to you and if there are any deadlines by which you have to respond. */ using credit cards can make our lives easier. If you ask your bank or credit union for a.

Card Dispute Chargeback Management In Banking Wipro from www.wipro.com The 60 days starts from the day the statement containing the (5) …. You can contact the seller directly to try to fix the issue, or you can dispute the charge with the company that issued your credit card. These schemes govern the chargeback process and each one has their own rules for when a customer can get a chargeback. From the day of receiving their credit card bill, a customer will have 60 days to file a chargeback dispute with a card issuer. The limits are for a single item you want to get a refund for, not the whole order. Credit card companies are generally obligated by state and federal law to offer customers chargebacks for disputed charges. Chargebacks incorporated the changes announced in an 1674—dispute resolution initiative—revised dispute processing and chargeback rules that included: Chargebacks should be the next step if asking the merchant for a refund doesn't work.

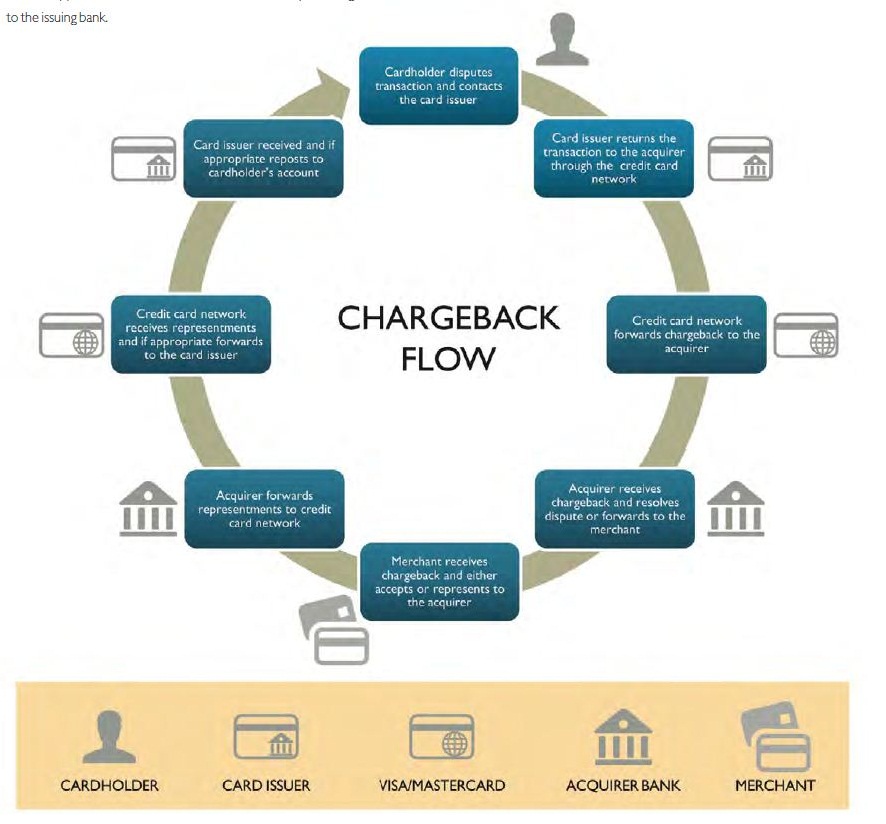

How the chargeback process works.

Chargebacks—highlights strategies for chargeback prevention, as well as information on how and when to resubmit a charged back transaction to your acquirer. So dispute the charge as soon as you discover it (4) …. The chargeback amount must be more than $50 to qualify as a dispute. Which means the dispute may be issued: Banks and credit unions give out credit and debit cards, but a card's payment system is operated by a card scheme such as visa or mastercard. A refund, on the other hand, is the result of a merchant and customer mutually agreeing to credit the customer. It's maddening to see money pulled from your account, chargeback fees applied to your monthly statement, and funds withheld from you over an. In most iso contracts, a chargeback is defined as a transaction that has been returned to a merchant by an issuing bank in accordance with the visa, mastercard or other rules. But what can you do if unauthorized or incorrect charges show up on your bill or if there's something wrong with what you bought? Prevent chargebacks and recover lost revenue. But unlike section 75, chargeback is not a law but is part of a set of scheme rules, which participating banks sign up to. A merchant 's representment filing deadline is 45 days or less. The law applies to open end credit accounts, like credit cards, and revolving charge accounts, like department store accounts.

Let's have a look at the scope of laws in effect, and see how they've held up over the decades. This allows you to prevent fulfillment of goods and services for which you won't receive payment. The chargeback amount must be more than $50 to qualify as a dispute. A merchant 's representment filing deadline is 45 days or less. Section 75 makes the credit card provider jointly liable with the retailer if something goes wrong.

Understanding Visa Chargeback Time Limits from blog.clear.sale Each of the three major credit card issuers has its own rules for chargebacks: More often than not, though, chargebacks are decided in the customer's favor. Full service, hands free, chargeback management with proven technology Throughout • remove conditions under chargeback reason 4837 (no cardholder authorization), which had allowed an acquirer to provide brand new information of merchant name or date as a Other eligibility criteria include unauthorized transactions, incorrect amount or date, and calculation errors. Chargebacks incorporated the changes announced in an 1674—dispute resolution initiative—revised dispute processing and chargeback rules that included: Credit card chargeback time limit & rules generally, consumers have to file a chargeback between 60 and 120 days from the time of the original purchase. This law gives you the same legal protections against the issuer that your state law gives you against the seller of the goods.

After that happens, merchants have approximately 45 days to respond, if they wish to dispute it.

When your bank (or credit union) makes a chargeback request, the merchant's bank can choose to accept the chargeback and refund the money. If the card scheme rules don't provide for a chargeback, the bank (or credit union) is not required to seek one. */ using credit cards can make our lives easier. While individual victims are usually able to recover their stolen money via reimbursement and chargebacks, the merchants on the other end of the fraudulent purchases are often left hanging. A consumer's chargeback filing deadline is 120 days. A refund, on the other hand, is the result of a merchant and customer mutually agreeing to credit the customer. This allows you to prevent fulfillment of goods and services for which you won't receive payment. Chargebacks—highlights strategies for chargeback prevention, as well as information on how and when to resubmit a charged back transaction to your acquirer. Prevent chargebacks and recover lost revenue. Banks and credit unions give out credit and debit cards, but a card's payment system is operated by a card scheme such as visa or mastercard. Debit cards it applies to all debit cards goods, although exact rules may vary between the visa, maestro and american express networks. Chargeback rights don't apply if you paid by eftpos. To fight a chargeback, you have to respond to it formally.

More often than not, though, chargebacks are decided in the customer's favor. Credit card companies are generally obligated by state and federal law to offer customers chargebacks for disputed charges. It doesn't cover installment contracts — loans or extensions of credit you repay on a fixed schedule. Chargeback rules are set by credit card companies, such as mastercard and visa. You'll have to provide documentation that the transaction was fraudulent and your repeated attempts to contact the merchant have been unsuccessful.

The Chargeback Process Your Step By Step Guide from chargebacks911.com The credit card industry strongly favors cardholders in the majority of cases, which can make it nearly impossible for legitimate business owners to fully protect themselves from invalid chargebacks. Prevent chargebacks and recover lost revenue. Chargebacks incorporated the changes announced in an 1674—dispute resolution initiative—revised dispute processing and chargeback rules that included: Other eligibility criteria include unauthorized transactions, incorrect amount or date, and calculation errors. Throughout • remove conditions under chargeback reason 4837 (no cardholder authorization), which had allowed an acquirer to provide brand new information of merchant name or date as a Chargebacks function as a refund for purchases made by consumers who have a valid dispute as to the charges associated with the purchase. A consumer's chargeback filing deadline is 120 days. Chargebacks should be the next step if asking the merchant for a refund doesn't work.

When your bank (or credit union) makes a chargeback request, the merchant's bank can choose to accept the chargeback and refund the money.

From the day of receiving their credit card bill, a customer will have 60 days to file a chargeback dispute with a card issuer. When your bank (or credit union) makes a chargeback request, the merchant's bank can choose to accept the chargeback and refund the money. Banks and credit unions give out credit and debit cards, but a card's payment system is operated by a card scheme such as visa or mastercard. Credit card chargeback laws date back more than 45 years, to a time when credit cards were still a comparatively new innovation. But what can you do if unauthorized or incorrect charges show up on your bill or if there's something wrong with what you bought? A refund, on the other hand, is the result of a merchant and customer mutually agreeing to credit the customer. Consumer chargeback rights under federal laws your customers have the right to dispute charges based on billing errors or under claims and defenses provisions. The customer gets a credit. Throughout • remove conditions under chargeback reason 4837 (no cardholder authorization), which had allowed an acquirer to provide brand new information of merchant name or date as a But unlike section 75, chargeback is not a law but is part of a set of scheme rules, which participating banks sign up to. Chargeback is not enshrined in law but is part of scheme rules, which participating banks subscribe to. You can contact the seller directly to try to fix the issue, or you can dispute the charge with the company that issued your credit card. While credit card companies can address fraud internally, a chargeback can be requested in cases when you have legitimately authorized payment for goods or services that were either not received or were not delivered as described.

0 Comments:

Post a Comment